Project: Learning to Adapt: Test-Time Normalization for Non-Stationary Time Series Forecasting

Description

Background & Motivation:

In real-world time series forecasting tasks—such as energy demand, traffic, or financial signals, data distributions often shift over time. These non-stationarities (e.g., changes in trend, seasonality, or noise) can significantly degrade model performance at test time.

Recent methods like RevIN (Reversible Instance Normalization) [1], SAN (Slicing Adaptive Normalization) [2], FAN (Frequency Adaptive Normalization) [3], and Dish-TS [4] use normalization to mitigate distributional shifts. However, these techniques typically apply fixed normalization during training or inference, without adapting to new test-time conditions.

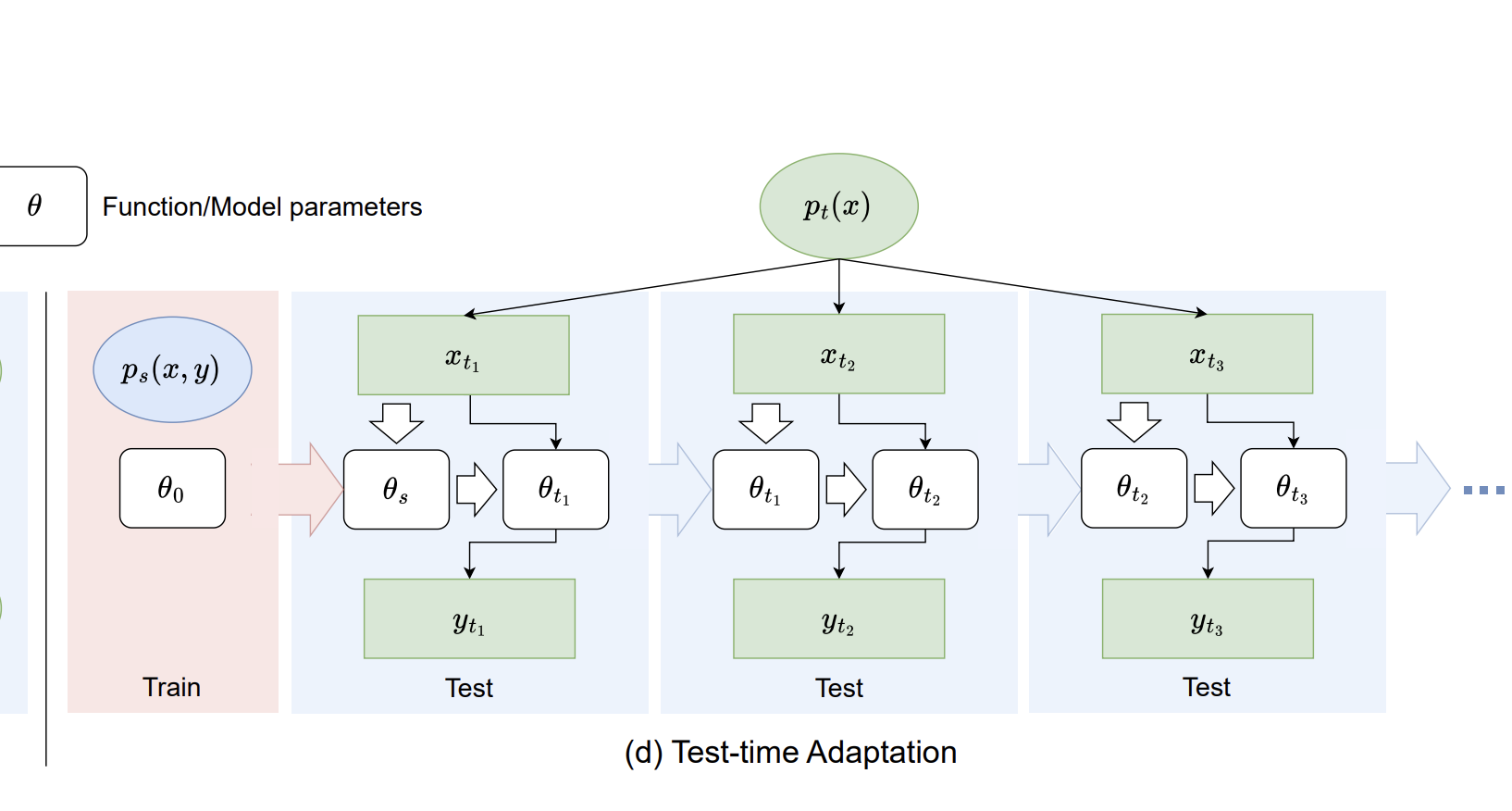

In contrast, test-time adaptation (TTA) [5], widely studied in vision and NLP, enables models to adjust dynamically to test inputs without labels. This concept remains less explored in time series forecasting.

This project investigates whether test-time normalization (TTN), inspired by TTA, can improve forecasting accuracy under non-stationary conditions by allowing the model to adapt to evolving input distributions at inference.

Objective:

* Do a literature review on test-time adaptation [5] techniques.

* Extend existing normalisation methods [1-4] to operate as online test-time adaptation modules.

* Explore fast statistics estimation and light updates from the test sequence (without labels).

* Evaluate benefits for continual or streaming forecasting tasks.

Contribution:

* A practical method for on-the-fly adaptation.

* Empirical insight into test-time shifts and how models can recover.

* Could lead to a low-cost, plug-and-play module for deployed models.

Students with experience in time series forecasting and a strong interest in research are encouraged to apply. This project has the potential to a publication.

[1] Kim, Taesung, et al. "Reversible instance normalization for accurate time-series forecasting against distribution shift." International conference on learning representations. 2021.

[2] Liu, Zhiding, et al. "Adaptive normalization for non-stationary time series forecasting: A temporal slice perspective." Advances in Neural Information Processing Systems 36 (2023): 14273-14292.

[3] Ye, Weiwei, et al. "Frequency Adaptive Normalization For Non-stationary Time Series Forecasting." arXiv preprint arXiv:2409.20371 (2024).

[4] Fan, Wei, et al. "Dish-ts: a general paradigm for alleviating distribution shift in time series forecasting." Proceedings of the AAAI conference on artificial intelligence. Vol. 37. No. 6. 2023.

[5] Xiao, Zehao, and Cees GM Snoek. "Beyond model adaptation at test time: A survey." arXiv preprint arXiv:2411.03687 (2024).

Details

- Student

-

NWNaijia Wan

- Supervisor

-

Amy Deng

Amy Deng